What is a Medicare Advantage Plan?

The Medicare Advantage Plan, also known as Medicare Part C, is a type of health insurance offered by private insurance companies that contract with the federal government to provide Medicare benefits to eligible individuals. It is an alternative to Original Medicare (Medicare Part A and B).

It typically includes additional benefits not covered under Original Medicare, such as prescription drug coverage and routine vision and hearing services. In this blog post, we’ll explain the Medicare Advantage Plan, how it works, and the benefits and limitations to consider when deciding if it’s the right choice for you.

How Does Medicare Advantage Plan Work?

Medicare Advantage Plans are an excellent option for those seeking an alternative to original Medicare. Medicare Advantage Plans, also known as Medicare Part C, are offered by private insurance companies that contract with the federal government to provide Medicare benefits to eligible individuals.

These plans provide an alternative to Original Medicare (Medicare Part A and Part B). They typically include additional benefits not covered under Original Medicare, such as prescription drug coverage and routine vision and hearing services.

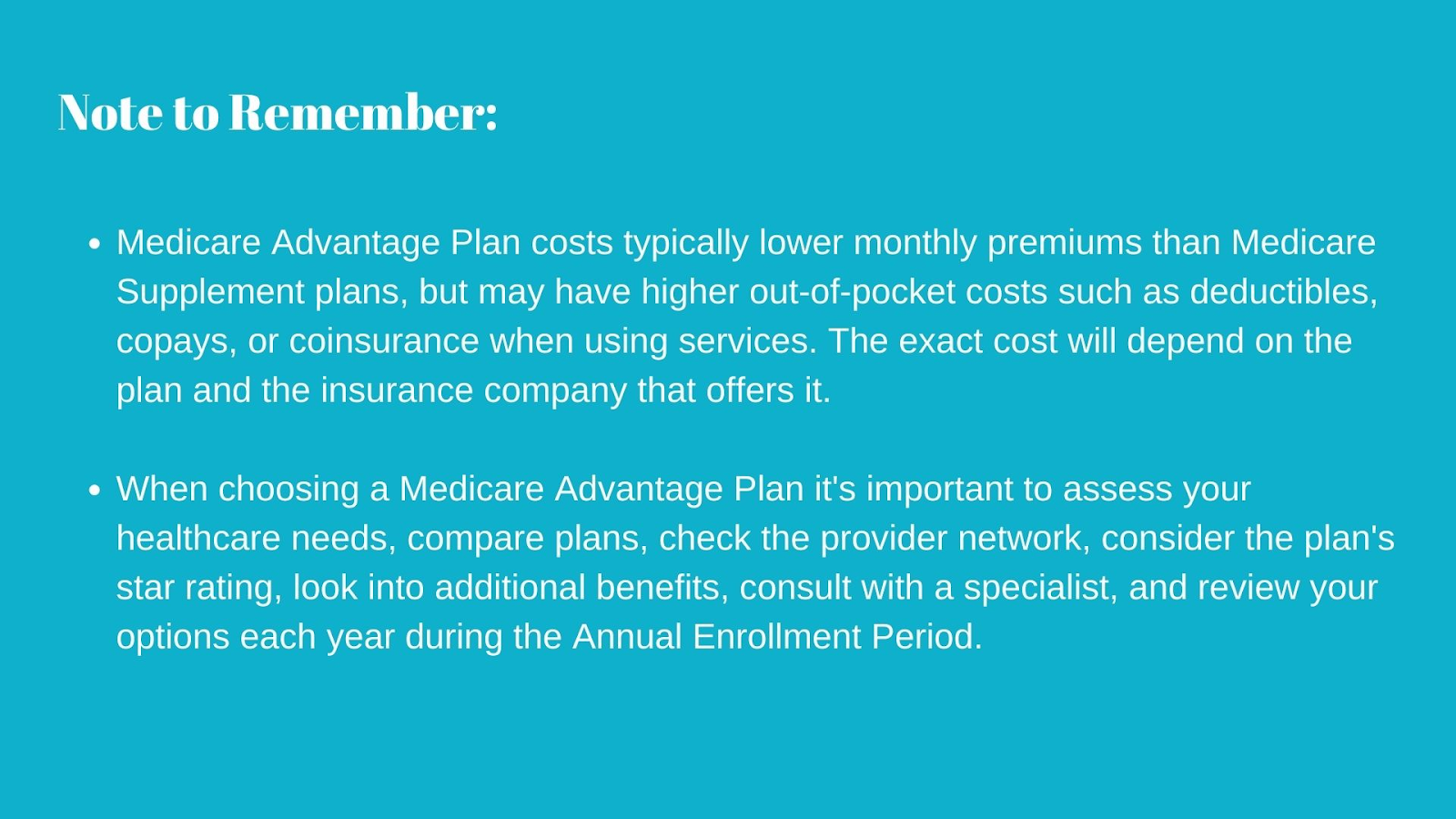

When you enroll in a Medicare Advantage Plan, you will receive your Medicare benefits through a private insurance company rather than the federal government. Your plan will have a network of providers you must use to cover your services. The plan will also have a monthly premium, typically lower than Medicare Supplement plans. You may also have out-of-pocket costs when you use services, such as co-pays or deductibles.

The private insurance company that manages your plan is also responsible for determining which services are covered and how much they will pay for each service. The Medicare Advantage Plan may require referrals to see specialists or limit the number of days in the hospital you can have covered.

You are still entitled to all of the benefits provided by Original Medicare if you choose to enroll in a Medicare Advantage plan. It is important to review the coverage details of your plan each year during the Annual Enrollment Period (AEP) between October 15th – December 7th to ensure you are still getting the best coverage for your specific healthcare needs.

What is a Medicare Advantage Coverage?

Medicare Advantage coverage is a great option for those looking to supplement their existing Medicare plans. Medicare Advantage Plans, also known as Medicare Part C, typically cover the same services as Original Medicare (Medicare Part A and Part B). Still, they also may include additional benefits not covered under Original Medicare, such as:

- Prescription drug coverage (Part D)

- Routine vision and hearing services

- Routine dental care

- Gym memberships

- Health and wellness programs

- Over-the-counter medication coverage

- Healthy Food card

The benefits offered by a specific Medicare Advantage Plan will vary depending on the plan and the insurance company. Some Medicare Advantage Plans also offer extra benefits such as transportation to medical appointments and coverage for foreign travel emergency care.

It is important to note that while some Medicare Advantage plans may offer additional benefits, they also may limit the coverage of certain services, such as limiting the number of days in the hospital you can have covered. Additionally, some plans may require referrals to see specialists or have other restrictions on covered services.

You need to review the coverage details of your plan each year during the Annual Enrollment Period (AEP – from Oct 15th to Dec 7th) to ensure you are still getting the best coverage for your specific healthcare needs. This can be done by comparing the coverage and costs of different plans and determining which one best meets your individual needs.

How Much Do Medicare Advantage Plans Cost?

Medicare Advantage Plans cost can vary depending on the plan and the insurance company that offers it. Medicare Advantage Plans typically have lower monthly premiums than Medicare Supplement plans, but they may have higher out-of-pocket costs plans vary; most plans may be at a Zero cost to you.

Here are some of the costs you may be responsible for when enrolled in a Medicare Advantage Plan:

- Monthly premium: This is the amount you pay the insurance company to participate in the plan. The premium is usually lower than Medicare Supplement plans.

- Deductible: This is the amount you must pay out-of-pocket before your plan begins to pay for covered services.

- Copays or Coinsurance: A copay is a fixed dollar amount you pay for a specific service, and coinsurance is a percentage of the cost of a service that you pay.

- Out-of-pocket maximum: This is the most you will have to pay for covered services in a calendar year. After you reach this amount, the plan will pay 100% of the covered services.

It’s important to note that not all of the above costs will be present in every Medicare Advantage Plan. Additionally, the cost of your plan may change each year and plan. It’s essential to review your plan’s costs and coverage details each year during the Annual Enrollment Period (AEP) and compare different plans to find the one that best meets your individual needs and budget.

Which is Better, Original Medicare or Medicare Advantage?

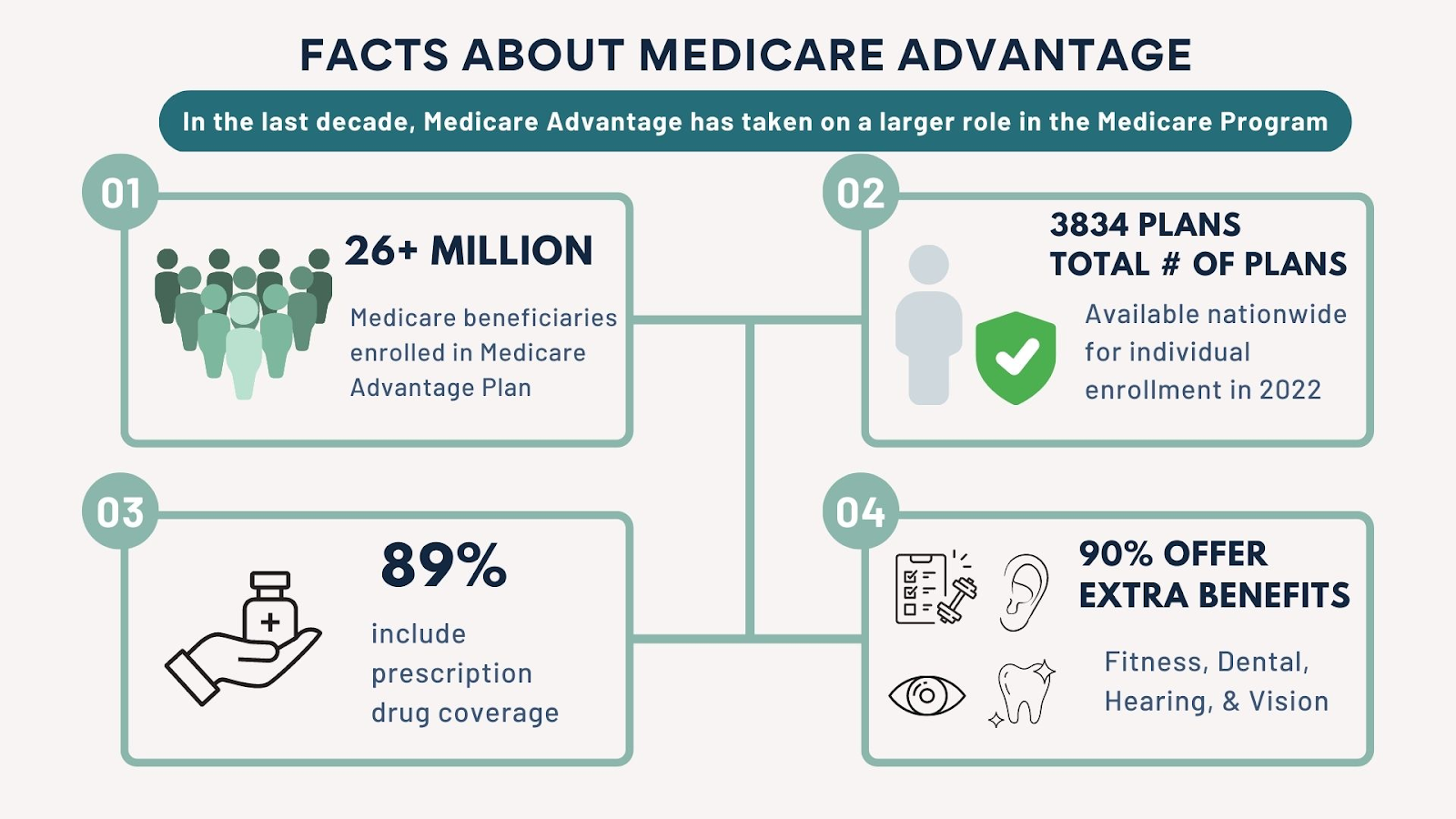

Medicare Advantage plans have become increasingly popular in recent years, with over 20 million Medicare beneficiaries enrolled in Medicare Advantage plans. Whether Original Medicare or a Medicare Advantage Plan is the better choice depends on your health care needs and budget. Original Medicare (Medicare Part A and Part B coverage) and Medicare Advantage Plans have their benefits and limitations.

Original Medicare provides a wide range of coverage for hospital and medical services, including inpatient care in hospitals, doctor services, lab tests, and certain preventive services. With Original Medicare, you can see any provider that accepts Medicare without the need to stay in-network. But, it does not cover certain benefits such as vision, dental, and hearing. You may purchase a separate policy or Medicare supplement insurance plan (Medigap) to cover these costs.

Medicare Advantage plans are an alternative to Original Medicare, offered by private insurance companies that contract with the federal government. Medicare Advantage Plans typically include additional benefits not covered under Original Medicare, such as prescription drug coverage and routine vision and hearing services.

Medicare Advantage Plans offer an alternative to Original Medicare for your health and drug coverage. These plans provide all of the coverage of Original Medicare, including Part A (Hospital Insurance) and Part B (Medical Insurance), as well as additional benefits such as vision, hearing, dental, or wellness coverage. Many plans also include prescription drug coverage. You may find that the network of providers is more limited than with Original Medicare, but you may pay less out-of-pocket costs when using services than with Original Medicare. When deciding between Original Medicare and a Medicare Advantage Plan, it is important to consider your healthcare needs and budget. Comparing the coverage and costs of different plans can help you make an informed decision and choose the best option. Reviewing the coverage details of your plan each year during the Annual Enrollment Period (AEP) can ensure that you have the best plan for your individual needs.

How to Choose the Right Medicare Advantage Plan for You?

Choosing the right Medicare Advantage Plan for you can be a complex process, as many different plans are available with varying coverage options and costs. Here are some steps you can take to help you choose the right plan for you:

- Assess your health care needs: Consider your current health and any chronic conditions. If you have specific healthcare needs, such as ongoing prescription drug coverage or routine vision and hearing services, look for plans that offer those benefits.

- Compare plans: Compare the coverage and costs of different plans. Look at the monthly premium, deductibles, copays, and out-of-pocket maximums.

- Check the provider network: Make sure the doctors, hospitals, and other providers you want to use are part of the plan’s network.

- Consider the plan’s star rating: Each Medicare Advantage Plan is rated by the Centers for Medicare and Medicaid Services (CMS) based on its quality and performance. The higher the star rating, the better the plan.

- Look into additional benefits: Some plans may offer additional benefits such as gym memberships, over-the-counter medication coverage, or transportation to medical appointments. If these are important to you, make sure your chosen plan offers them.

- Confirm that your Medications are covered: If you are already taking medications, check the formulary(list of covered drugs) and make sure that your medications are covered by the plan you are considering.

- Consult an agent or a broker: They can help you compare different plans and guide you through enrollment.

- Review your options: During the Annual Enrollment Period, review the coverage and cost of Medicare advantage plan and compare it to other available plans. See if the new plan best suits your needs and budget.

What is the Enrollment Period for Medicare Advantage Plans?

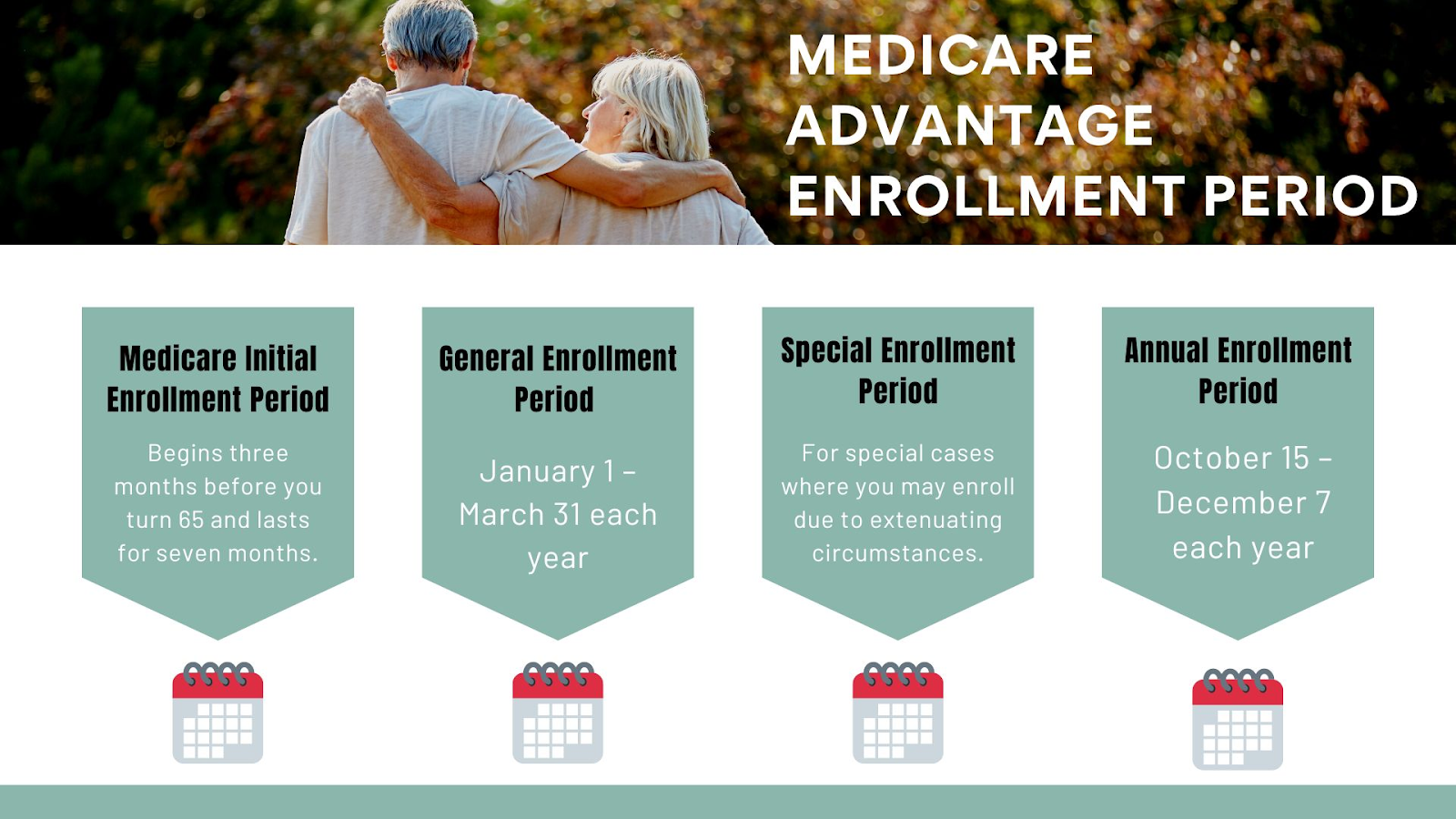

The Medicare Advantage Plan enrollment period, also known as Medicare Part C, is called the Annual Enrollment Period (AEP). The AEP runs from October 15th to December 7th each year. During this time, individuals already enrolled in a Medicare Advantage Plan can switch to a different plan or switch back to Original Medicare. Individuals currently enrolled in Original Medicare can also enroll in a Medicare Advantage Plan during this time.

It’s important to note that if you want to switch to a different Medicare Advantage Plan or switch from a Medicare Advantage Plan back to Original Medicare during the Annual Enrollment Period, your new coverage will begin on January 1st of the following year.

There are also other enrollment periods for Medicare Advantage that you should be aware of:

- Initial Enrollment Period (IEP): The IEP is the seven-month period that begins three months before the month you turn 65, includes the month you turn 65, and ends three months after the month you turn 65. During this time, you can enroll in a Medicare Advantage Plan for the first time.

- Special Enrollment Period (SEP): You may be eligible for a SEP if you have certain life-changing events such as moving out of the plan’s service area, losing employer coverage, or gaining or losing Medicaid eligibility. The SEP allows you to enroll in, or switch between, Medicare Advantage Plans or switch back to Original Medicare outside of the Annual Enrollment Period.

It is important to note that if you wait to enroll during your Initial Enrollment Period or Special Enrollment Period, you may have to pay a late-enrollment penalty and be limited in your options.

Who Can Join a Medicare Advantage Plan?

To join a Medicare Advantage Plan, also known as Medicare Part C, you must:

- Be enrolled in Medicare Part A (Hospital Insurance) and Part B (Medical Insurance)

- Live in the service area of the Medicare Advantage plan you wish to join

- Beginning in 2021, people with End-Stage Renal Disease (ESRD) can enroll in Medicare Advantage Plans. Medicare Advantage Plans