What Do I Need to Do Before Turning 65?

Do you know what you need to do before turning 65? At age 65, you may have various plans and aspirations, such as spending time with grandchildren, retiring, or taking a long-awaited trip. However, 65 also marks an important milestone for your healthcare as it is the age when you become eligible for Medicare coverage options.

Medicare is a government-funded health insurance program that provides hospital insurance (Part A) and medical insurance (Part B) to individuals 65 and older and those under 65 with a qualifying disability. Together, Part A and Part B are known as Original Medicare. While enrolling in Medicare is important, you should do a few other things before signing up. This blog post will guide you through everything you need to do to get ready for Medicare. So let’s get started!

Do I Need to Sign up for Medicare Before Turning 65?

Turning 65 is a big milestone, and if you’re receiving Social Security benefits or certain other government services, you may already be enrolled in Medicare Parts A and B. However, in some situations, such as being disabled or part of a qualified employer plan, you’ll have to enroll manually. If you’re not receiving Social Security benefits, you’ll need to sign up for Medicare during the seven-month period that begins three months before your 65th birthday.

It’s important to sign up for Medicare before you reach age 65 to ensure your coverage won’t be delayed so that you don’t miss important deadlines. If it’s determined that you do need to sign up manually, contact your state Medicare office or social security administration office for more details on how to enroll.

What to Do 6 Months Prior to Turning 65?

With turning 65 just around the corner, it’s crucial to get your Medicare health insurance plan in order. Six months before you turn 65, you should begin researching the benefits and programs best for you. Depending on what state you live in, there may be different options available when it comes to supplemental or private insurance.

Six months before you turn 65 is a good time to start thinking about enrolling in Medicare.

So, what to do for Medicare before turning 65? Here are a few things you can do to prepare:

- Determine your eligibility: You’ll be eligible for Medicare if you’re 65 or older and a U.S. citizen or permanent legal resident who has lived in the United States for at least five consecutive years.

- Review your existing coverage: If an employer-sponsored health plan currently covers you, check with your employer or union to see how Medicare will affect that coverage.

- Learn about the different parts of Medicare: Medicare is divided into four parts: Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage), and Part D (drug coverage). Learn about each of these parts and the coverage they provide so you can decide which options are best for you.

- Research your coverage options: There are several different ways to get coverage through Medicare, including Original Medicare (Parts A and B), Medicare Advantage (Part C), and Medicare Supplement (Medigap) plans. Research the options available and compare the costs, benefits, and coverage provided.

- Make a note of your Initial Enrollment Period: It starts three months before your 65th birthday, including the month of your birthday, and lasts for seven months. That is a time you will have to enroll in Medicare if you haven’t enrolled automatically through Social Security.

- Organize your documents: Gather your personal information, such as your Social Security number and birth date, as well as any information about your current coverage. This will make it easier to enroll in Medicare when the time comes.

It’s always important to plan and gather information to make the best choices for yourself. If you have any doubts, don’t hesitate to contact the Social Security Administration or Medicare’s customer service.

How to Sign up for Medicare Before Turning 65?

Signing up for Medicare at the right time can be a straightforward process, though turning 65 is not always the ideal time to enroll. Recent retirees may want to take advantage of Medicare Part D – an optional prescription drug program–or enroll during their next open enrollment period to reduce premiums or deductibles.

Those turning 65 should start by looking at the eligibility requirements online or speaking with a human resources representative from their job if they’re not yet retired. Then, one must complete parts A and B of the application enrollment form before turning 65 and receiving a health insurance card from Social Security.

If you’re under the age of 65 and eligible for Medicare due to a disability or a certain medical condition, you can sign up for Medicare during your Initial Enrollment Period (IEP).

Here’s how to sign up for Medicare turning 65:

- Visit the Social Security Administration’s website at www.ssa.gov to apply online.

- Call the Social Security Administration at 1-800-772-1213 to make an appointment to apply in person.

- Contact your local Social Security office to schedule an appointment to apply in person.

- If you worked for a railroad, you could apply for Medicare through the Railroad Retirement Board at 1-877-772-5772

When you apply, you must provide proof of your age, citizenship or legal residency, and other required documents.

Remember that if you receive disability benefits from Social Security, you will automatically be enrolled in Medicare after 24 months, starting from the first disability payment. If you have Amyotrophic Lateral Sclerosis (ALS), you will be automatically enrolled in Medicare in the first month of your disability benefit period.

Those turning 66 also have ten months to sign up for Medigap coverage, which provides additional coverage for out-of-pocket costs associated with Medicare Part A and Part B expense-sharing plans. Finally, turning 65 doesn’t mean losing other insurance like employer plans, but it is important to check if these meet all the requirements set out by Medicare first.

What Are the Benefits of Turning 65?

Reaching the age of 65 has many benefits. So, what are the benefits of turning 65? For starters, benefits such as Medicare and Social Security become available to US citizens and those eligible for citizenship who have lived in the US for at least five years. Additionally, discounts such as a reduction in taxes are offered at restaurants, theaters, stores, and other establishments to those aged 65 and older.

Furthermore, many workers also receive benefits such as pensions when they reach this age which helps contribute towards their retirement fund. Therefore turning 65 offers additional financial support and reduces costs with benefits available to those entering this stage of life.

What is the Enrollment Period for Medicare When Turning 65?

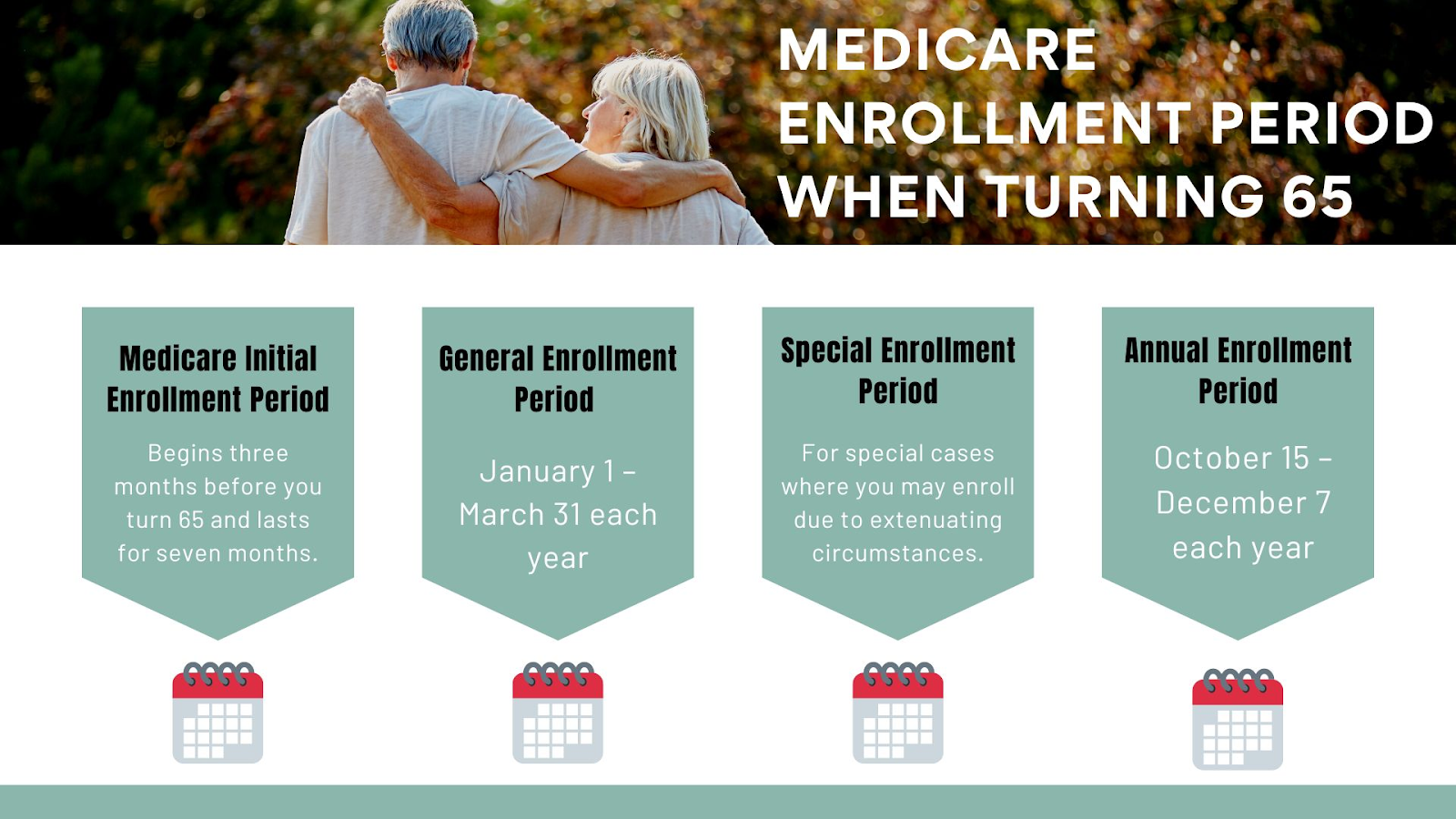

When turning 65, Medicare enrollment starts, and it can be challenging to know when and how to enroll in Medicare. The Initial Enrollment Period (IEP) for Medicare is a seven-month period that begins three months before your 65th birthday, includes your birthday month, and ends three months after your birthday month. This is when you can enroll in Medicare for the first time if you are not already receiving benefits through Social Security.

It is important to note that if you fail to enroll during your IEP, you may have to pay a late-enrollment penalty and face a coverage gap.

There is also an Annual Enrollment Period (AEP) for Medicare Advantage and Medicare Prescription Drug plans. It is from October 15 through December 7 each year. You can change your Medicare Advantage and Prescription Drug plan coverage during this period or switch back to Original Medicare with a Medigap policy. Changes you make during the AEP will take effect on January 1 of the following year.

Also, Special Enrollment Periods (SEP) allow you to change your coverage outside the Annual Enrollment Period. Special Enrollment Periods are triggered by specific events, like moving out of the coverage area of your current plan or if your current plan stops offering coverage. If a special event applies to you, you may be eligible for a SEP, which allows you to make changes to your coverage.

It’s important to review your options and understand your coverage during these periods to ensure you have the coverage you need when you need it.

When Turning 65, When Does Medicare Coverage Start?

Turning 65 is an exciting milestone- you’ve reached retirement age and now get the opportunity to explore all that life has to offer! When turning 65, it’s easy to think about the benefits of having more free time and less stress. But an important aspect of turning 65 is understanding when Medicare coverage starts. You can say turning 65 and Medicare is a combination!

If you are already receiving Social Security benefits, your Medicare coverage will begin automatically on the first day of the month you turn 65.

Suppose you are not receiving Social Security benefits and sign up for Medicare during your Initial Enrollment Period, which is the seven months starting three months before your 65th birthday. In that case, your coverage will begin one of two ways:

- Part A (hospital insurance) will start the first day of the month you turn 65 if you enroll in that month. Otherwise, it will start on the 1st day of the next month.

- Part B (Medical Insurance) starts the first day of the month after you enroll if you enroll on or before the end of the month before your 65th birthday. If you enroll in the month of your 65th birthday or after, it starts the first day following the month you enroll

- Part C Medicare Part C, also known as Medicare Advantage, is a type of Medicare health plan offered by private insurance companies that contract with Medicare. It provides all the benefits covered under Original Medicare.

For example, if your birthday is on July 15 and you sign up for Medicare during your initial enrollment period, your Part A coverage would begin on July 1, and your Part B coverage would begin on August 1.

It’s important to note that if you don’t sign up for Part B when you’re first eligible, you may have to pay a late-enrollment penalty when you do sign up, and if you don’t sign up for Medicare Part B when you’re first eligible, you may also face a gap in your coverage. It’s important to sign up during your initial enrollment period to avoid penalties and gaps in coverage.

Is a 65-Year-Old Without Medicare Eligible for Tricare?

So, what about Tricare and Medicare when turning 65? Tricare is a health insurance program for active duty and retired military members and their families. If you are 65 and are not enrolled in Medicare, you may be eligible for Tricare, depending on your circumstances.

Tricare for Life (TFL) is an option for Medicare-eligible military retirees and their dependents enrolled in Medicare Part A, and Part B. TFL acts as a secondary payer to Medicare, covering many out-of-pocket expenses not covered by Medicare. If you are a retiree, you would need to be enrolled in Medicare parts A and B to be eligible for TFL.

Suppose you are not a retiree but a military dependent. In that case, you may be eligible for Tricare Young Adult (TYA), a premium-based Tricare plan available to certain young adults who are no longer eligible to be covered under their sponsor’s Tricare coverage. But this will change if you reach 65 years old. At that point, you will have to have Medicare to continue with Tricare Young Adult.

Tricare Reserve Select (TRS) is a premium-based health plan for certain members of the Selected Reserve, including the National Guard. Eligibility requirements and benefits for TRS differ from those for TFL or TYA.

It’s important to check with the Department of Defense or a TRICARE Service Center to confirm your eligibility and to understand the specific coverage options and costs associated with Tricare for people over 65.

What Are the Alternatives to Original Medicare When Turning 65?

Medicare and turning 65 always sit together. When you reach the age of 65 and become eligible to enroll in Medicare, you may choose to supplement your Original Medicare (Part A and Part B) coverage with additional options. These could include:

- Medicare Supplement Insurance (Medigap) Plans: Medicare Supplement insurance plans to assist with the payment of out-of-pocket expenses such as copayments, coinsurance, and deductibles. You have a six-month open enrollment period for Medicare Supplements that begins when you turn 65 and are enrolled in Medicare Part B.

- Medicare Part D: Prescription drug coverage is provided under Medicare Part D. Original Medicare does not cover the majority of prescription pharmaceuticals taken at home, which is why some Medicare seniors choose Part D coverage. You have a 7-month Initial Enrollment Period for Part D that begins three months before your 65th birthday, includes your 65th birthday, and ends three months after your 65th birthday.

- Medicare Advantage is a private insurance company-provided alternative to getting your Part A and B benefits. Except for hospice care, which is still covered by Medicare Part A, Medicare Advantage plans must cover everything that Medicare Part A and Part B cover. The Medicare Advantage Initial Enrollment Period is the same as the Medicare Part D Initial Enrollment Period, which is seven months. It begins three months before your 65th birthday, including your 65th birthday month, and concludes three months after your 65th birthday.

Medicare Part C, also known as Medicare Advantage, offers a number of benefits compared to Original Medicare (Part A and Part B), including:

- Additional benefits: Many Medicare Advantage plans include additional benefits such as vision, hearing, and dental coverage, which are not covered by Original Medicare.

- Prescription drug coverage: Most Medicare Advantage plans include prescription drug coverage (Medicare Part D) as part of the plan.

- Lower out-of-pocket costs: Some Medicare Advantage plans have lower out-of-pocket costs, such as copayments, coinsurance, and deductibles, than Original Medicare.

- Network providers: Medicare Advantage plans have networks of providers that beneficiaries must use in order to receive coverage. This can be beneficial for beneficiaries who want the peace of mind of knowing that their providers are covered.

- Coordination of care: Medicare Advantage plans often coordinate care for beneficiaries with chronic conditions to help them manage their health more effectively.

- No referral needed to see a specialist: With Medicare Advantage, beneficiaries don’t need a referral from their primary care physician to see a specialist.

It’s important to note that Medicare Advantage plans can vary by location and by an insurance company, so beneficiaries should compare the benefits and costs of different plans before enrolling.

Comparing Plans is easy; you can check by using your zip code

Thoughts

Retirement is a big life change, but it doesn’t have to be stressful. If you plan and make some important decisions about your finances, health insurance, and living arrangements, you can set yourself up for a smooth transition into this new stage of life. As you approach the age of turning 65, it’s important to start thinking about your healthcare options and how they may change.

Once you’ve become a proud holder of your Medicare card and acquired both Parts A & B, reach out to us so we can explore the unique health plan options best suited for you.

You will want to determine your Medicare eligibility and understand the program’s different parts and the coverage they provide. This will help you make an informed decision about which options are best for you. So start planning now and enjoy your well-earned retirement! And if you have any questions, our team of experts is always available to help.

Skip to content

Skip to content