The health insurance plan known as Tricare for Life (TFL) is available to qualifying military retirees and their eligible dependents. Medicare, the federal health care program for many Americans 65 and older and those with specific disabilities, differs from this.

Tricare and Medicare will collaborate to provide your health benefits if you’re among the numerous military retirees. Together, Medicare and Tricare will make it easier for many military retirees to access high-quality healthcare services while lowering or eliminating many out-of-pocket expenses.

How Are Tricare and Medicare Different?

Federal health insurance programs include Tricare for Life and Original Medicare, often known as Medicare Parts A and B. When a service person or family member has Original Medicare, Tricare for Life is supplemental insurance.

One of the main distinctions between Tricare for Life and Original Medicare is that the former assists with covering your out-of-pocket expenses that Original Medicare does not, such as copays and coinsurance.

Everyone in the United States who is eligible for Medicare and Tricare can access it. Still, Tricare for Life offers Medicare-wraparound coverage to Tricare members who are also covered by Medicare Part A and Part B from enrollment fees.

Here’s A More Detailed Comparison of Both Medicare and Tricare life coverage

Tricare:

The National Guard, Reserves, and active duty service personnel’ families are covered by Tricare, a health insurance program offered by the federal government. Additionally, it is accessible to select former wives, survivors, and family members of retired military personnel worldwide.

Medicare:

Medical insurance is provided by Medicare Part B, whereas hospital insurance is provided by Medicare Part A. These Part A and Part B expenditures are covered by private plans, including Medicare Advantage, Medicare Part D plans, and Medigap, with additional benefits, prescription coverage, and out-of-pocket expenses.

Which Plan Between Medicare and Tricare for Life Covers More Services?

The insurance provider is expected to provide all of the same benefits as standard Medicare, and many programs also provide extra services. Depending on the policy, these extras could include prescription medicine, vision, dental, and hearing coverage. Absolutely, you can select a Medicare Advantage plan if you have TRICARE for Life. It’s crucial to understand the potential effects of having both policies, though.

These factors consist of:

Insurance for prescription drugs:

TRICARE provides prescription medicine coverage for Life. Likewise, a lot of Medicare Advantage plans. If you don’t want dual coverage, you might select a Medicare Advantage plan without prescription medication coverage, which would probably result in a lower monthly payment.

Provider networks.

If you use in-network providers for Medicare Advantage, you’ll typically save the most money. This network is normally smaller than you would get with original Medicare or TRICARE for Life.

Costs.

There are Medicare Advantage plans with no monthly fees and those without. When you visit in-network doctors, most plans will demand that you make a copayment. Medicare and TRICARE for Life frequently covers the cost of these copayments.

What Are the Benefits of Having Both Tricare and Medicare?

Tricare For Life and Medicare can provide a wide range of health care benefits. In addition to the expanded coverage options offered by Medicare, Tricare can supplement this insurance with additional medical services such as long-term care or vision and dental coverage for retirees. With both plans, individuals will have access to more medical services that may otherwise not be covered under either plan alone.

Furthermore, those with both plans may also benefit from cost savings on out-of-pocket expenses or co-payments typically required when receiving specific medical treatments. It is essential to consider all available options and compare costs before deciding which combination of plans best meets an individual’s needs.

Can You Still Receive Tricare if You Have Medicare?

TRICARE automatically covers you For Life if you have Medicare Parts A and B. TRICARE For Life.

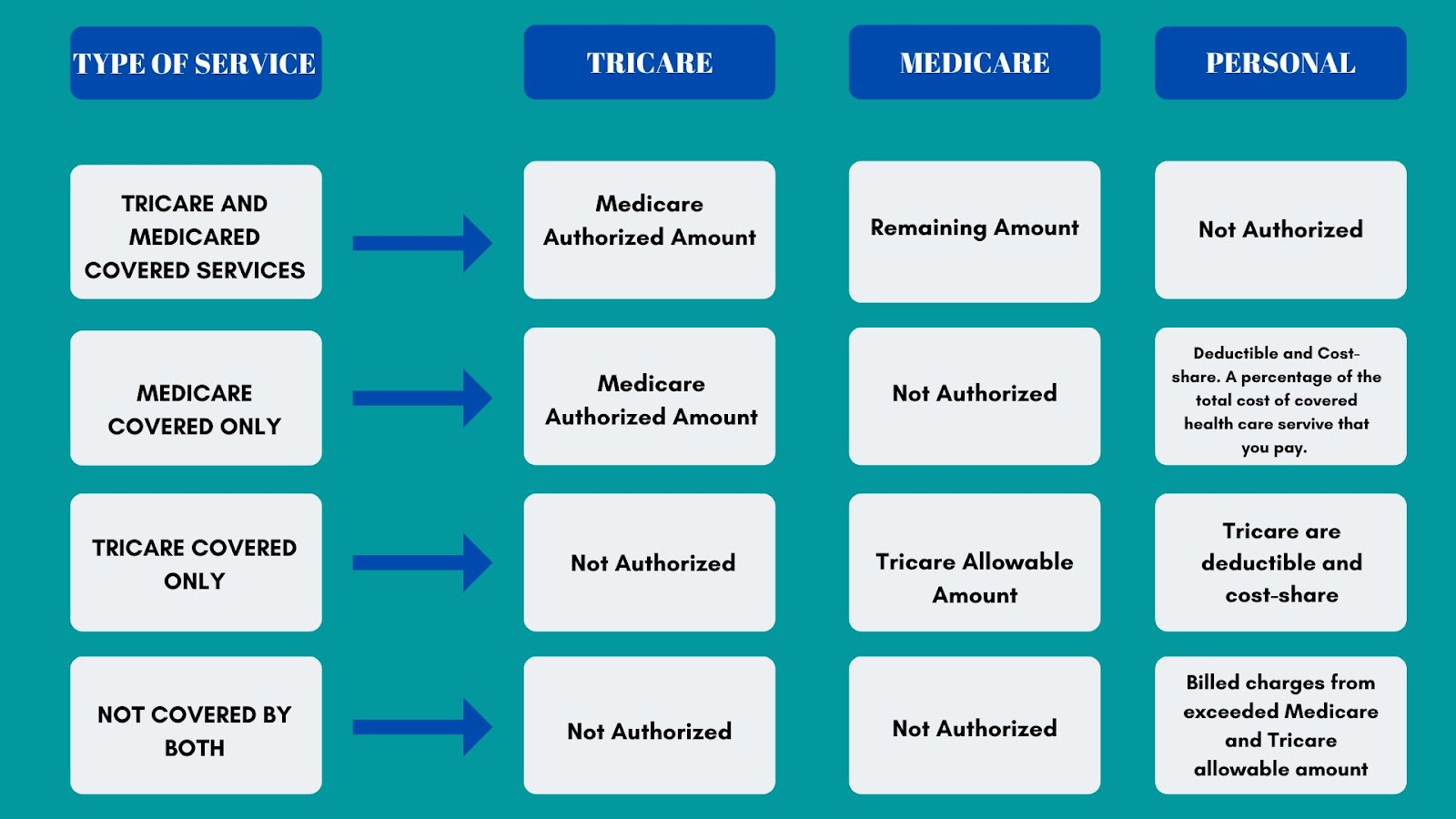

Your primary payer is Medicare. If you have additional health insurance in addition to TRICARE, such as Medicare or employer-sponsored health insurance, TRICARE pays last or second to last to Medicare. Supplements to TRICARE are not considered “other health insurance.”

For services covered by TRICARE and Medicare, TRICARE benefits include paying the coinsurance and deductible of Medicare. Retired service members and eligible family members who turn 65 and become eligible for Medicare are then automatically eligible for TRICARE For Life. They are no longer allowed to sign up for other TRICARE plans.

Who is Eligible for Tricare and Medicare?

Tricare and Medicare advantage eligibility requirements vary depending on a person’s military service history or current affiliation with the armed forces. Generally speaking, those currently serving in the military, retired service members and their families, and survivors of deceased veterans may be eligible for Tricare coverage. On the other hand, Medicare is available to most people over 65 years old and individuals with specific disabilities. Additionally, some low-income individuals may qualify regardless of age. It is important to review each plan’s details separately before deciding when selecting health care coverage.

- Active Duty Service Members

- Active Duty Family Members

- Retired Service Members and Family Members

- TRICARE Reserve Select

- TRICARE Retired Reserve

- US Family Health Plan

- Those Who Don’t Qualify for Medicare Part A

How To Choose The Right Coverage For You?

Determining the services you want or need might help you choose the insurance policy that works best for you. TRICARE for Life may greatly decrease your out-of-pocket expenses, but it might still not cover all of the services that Medicare Advantage does.

Additionally, you can acquire extra insurance from private insurance providers, such as Medicare Part D plans or Medicare supplement insurance. All of these, Medicare and Tricare for life coverage could assist in lowering your overall healthcare expenses.

What are the Medicare Prescription Drug Coverage and Tricare?

If you have Tricare, you do not need Medicare prescription drug coverage since Tricare provides prescription medication coverage that goes above and above what is required by law. You can acquire coverage without signing up for a Medicare Advantage plan that offers prescription medication coverage or a separate Medicare Part D prescription drug plan.

Beyond what is mandated by law, Tricare offers benefits for prescription drug coverage. A Medicare Advantage Prescription Drug plan that combines medical and prescription drug benefits into one plan is not required for Tricare beneficiaries. A Medicare Advantage plan without prescription medication coverage is an option.

Some of these Medicare plans could be affordable, allowing you to keep paying your Part B payment while paying nothing for Medicare Advantage. As long as the pharmacy you use is included in the Medicare Advantage Prescription Drug plan and the Tricare networks of participating pharmacies, both Medicare and Tricare for life coverage programs will cover their respective portions of your covered prescription drug costs if you enroll in a Medicare Advantage Prescription Drug plan.

Which Plan is Better for Seniors?

The Medicare program will offer the least expensive health insurance with the best benefits for those 65 years of age or older or with a qualifying disability. When employed, you contributed to the Medicare program by paying an income tax on Medicare. The best time to profit from this investment is when you are in your senior years.

Medicare is divided into various components, including a public option offered through the Medicare administration and options provided by commercial insurance firms. With so many options, you can select the best suits your needs.

Why Are Tricare and Medicare Important?

Health insurance plans, such as Medicare and Tricare, are essential medical coverage options for seniors because they provide valuable healthcare benefits such as access to doctors, specialists, and medications that would otherwise be too costly to afford. These plans help seniors cover the financial burden of expensive medical treatments and can provide peace of mind knowing that health care is available when needed. Additionally, Medicare and Tricare offer access to specialized services such as home care or long-term care to help seniors stay independent.

Medicare and Tricare are important health insurance plans for seniors because they provide quality medical coverage options. Medicare is a federal health insurance program that offers hospital and medical benefits to people aged 65 and older. At the same time, Tricare is a health plan created specifically for U.S. military personnel and their families.

Thoughts

Benefits from Medicare Advantage and Tricare will be coordinated to reduce your out-of-pocket expenses for covered services. However, neither Tricare nor a Medicare Advantage plan will pay for specific therapies that are not medically required.

Senior Health Advisors are always available to help customers understand their options, choose the appropriate plan, and understand how it operates.